HOUSTON, Oct. 16, 2019 (GLOBE NEWSWIRE) — Crown Castle International Corp. (NYSE: CCI) (“Crown Castle”) today reported results for the quarter ended September 30, 2019, and issued its full year 2020 Outlook as reflected in the table below:

| (in millions) | Midpoint of Current Full Year 2020 Outlook |

Midpoint of Current Full Year 2019 Outlook |

Full Year 2018 Actual |

Full Year 2019 Outlook to Full Year 2020 Outlook % Change |

Full Year 2018 to Full Year 2019 Outlook % Change |

|||||

| Site rental revenues | $5,219 | $4,965 | $4,716 | +5% | +5% | |||||

| Net income (loss) | $1,128 | $926 | $671 | +22% | +38% | |||||

| Net income (loss) per share—diluted(a) | $2.53 | $1.95 | $1.34 | +30% | +46% | |||||

| Adjusted EBITDA(b) | $3,592 | $3,408 | $3,141 | +5% | +9% | |||||

| AFFO(a)(b) | $2,685 | $2,479 | $2,274 | +8% | +9% | |||||

| AFFO per share(a)(b) | $6.33 | $5.94 | $5.48 | +7% | +8% | |||||

(a) Attributable to CCIC common stockholders.

(b) See “Non-GAAP Financial Measures, Segment Measures and Other Calculations” included herein for further information and reconciliation of this non-GAAP financial measure to net income (loss).

“We delivered terrific results in the third quarter and increased our annualized common stock dividend by 7% to $4.80 per share,” stated Jay Brown, Crown Castle’s Chief Executive Officer. “We believe our ability to offer towers, small cells and fiber solutions, which are all integral components of communications networks and are shared among multiple tenants, provides us the best opportunity to generate significant growth while delivering high returns for our shareholders. Further, we believe that the U.S. represents the best market in the world for communications infrastructure ownership, and we are pursuing that compelling opportunity with our comprehensive offering.

“In 2019, we are experiencing the highest level of tower leasing activity in more than a decade, and we expect to generate a similar level of new leasing activity from towers in 2020 as our customers deploy additional cell sites and spectrum in response to the rapid growth in mobile data traffic. Additionally, we are constructing small cells for our customers as they invest in their current networks while beginning the early stages of 5G deployments, and we expect to deploy a similar volume of small cells in 2020 as we are deploying in 2019. With the positive momentum we continue to see in our Towers and Fiber segments, we remain focused on investing in our business to generate future growth while delivering dividend per share growth of 7% to 8% per year.”

RESULTS FOR THE QUARTER

The table below sets forth select financial results for the three month period ended September 30, 2019 and 2018.

| (in millions) | Q3 2019 | Q3 2018 | Change | % Change | ||||

| Site rental revenues | $1,260 | $1,184 | +$76 | +6% | ||||

| Net income (loss) | $272 | $164 | +$108 | +66% | ||||

| Net income (loss) per share—diluted(a) | $0.58 | $0.33 | +$0.25 | +76% | ||||

| Adjusted EBITDA(b) | $882 | $793 | +$89 | +11% | ||||

| AFFO(a)(b) | $646 | $579 | +$67 | +12% | ||||

| AFFO per share(a)(b) | $1.55 | $1.39 | +$0.16 | +12% | ||||

(a) Attributable to CCIC common stockholders.

(b) See “Non-GAAP Financial Measures, Segment Measures and Other Calculations” included herein for further information and reconciliation of this non-GAAP financial measure to net income (loss).

HIGHLIGHTS FROM THE QUARTER

- Site rental revenues. Site rental revenues grew approximately 6.4%, or $76 million, from third quarter 2018 to third quarter 2019, inclusive of approximately $70 million in Organic Contribution to Site Rental Revenues and an approximately $6 million increase in straight-lined revenues. The $70 million in Organic Contribution to Site Rental Revenues represents approximately 6.0% growth, comprised of approximately 9.7% growth from new leasing activity and contracted tenant escalations, net of approximately 3.7% from tenant non-renewals.

- Net income. Net income for the third quarter 2019 was $272 million, compared to $164 million during the same period a year ago.

- Capital expenditures. Capital expenditures during the quarter were $540 million, comprised of $18 million of land purchases, $29 million of sustaining capital expenditures, $491 million of discretionary capital expenditures and $2 million of integration capital expenditures. The discretionary capital expenditures of $491 million includes $371 million attributable to Fiber and $120 million attributable to Towers.

- Common stock dividend. During the quarter, Crown Castle paid common stock dividends of $1.125 per common share, an increase of approximately 7% on a per share basis compared to the same period a year ago.

- Financing activities. During the quarter, Crown Castle issued $900 million of Senior Unsecured Notes, with net proceeds from the offering and cash on hand used to repay outstanding indebtedness under the revolving credit facility and commercial paper program.

“The strong third quarter results reflect our ability to leverage our leadership position in the U.S. across towers, small cells and fiber solutions to generate attractive growth,” stated Dan Schlanger, Crown Castle’s Chief Financial Officer. “As we focus on closing out another successful year of growth in 2019 and look toward 2020, we are excited about the positive growth trends driving demand for our tower and fiber assets. During the last five years, and inclusive of the dividend increase we are announcing today, we have increased our dividend by a compounded annual growth rate of approximately 8%. Looking forward, we believe we are in a great position to deliver on our annual dividend growth target of 7% to 8% while at the same time making significant investments in our business that we believe will generate attractive long-term returns and support future growth.”

OUTLOOK

This Outlook section contains forward-looking statements, and actual results may differ materially. Information regarding potential risks which could cause actual results to differ from the forward-looking statements herein is set forth below and in Crown Castle’s filings with the SEC.

The following table sets forth Crown Castle’s current Outlook for full year 2019 and full year 2020:

| (in millions) | Full Year 2019 | Full Year 2020 | ||||||||

| Site rental revenues | $4,950 | to | $4,980 | $5,196 | to | $5,241 | ||||

| Site rental cost of operations(a) | $1,442 | to | $1,472 | $1,482 | to | $1,527 | ||||

| Net income (loss) | $896 | to | $956 | $1,088 | to | $1,168 | ||||

| Adjusted EBITDA(b) | $3,393 | to | $3,423 | $3,569 | to | $3,614 | ||||

| Interest expense and amortization of deferred financing costs(c) | $674 | to | $704 | $691 | to | $736 | ||||

| FFO(b)(d) | $2,363 | to | $2,393 | $2,539 | to | $2,584 | ||||

| AFFO(b)(d) | $2,464 | to | $2,494 | $2,662 | to | $2,707 | ||||

| Weighted-average common shares outstanding – diluted(e) | 418 | 424 | ||||||||

(a) Exclusive of depreciation, amortization and accretion.

(b) See reconciliation of this non-GAAP financial measure to net income (loss) and definition included herein.

(c) See reconciliation of “components of current outlook for interest expense and amortization of deferred financing costs” herein for a discussion of non-cash interest expense.

(d) Attributable to CCIC common stockholders.

(e) The assumption for diluted weighted-average common shares outstanding for full year 2019 Outlook is based on the diluted common shares outstanding as of September 30, 2019, and does not include any assumed conversion of preferred stock in the share count. The full year 2020 Outlook is inclusive of the assumed conversion of preferred stock in August 2020, which we expect to result in (1) an increase in the diluted weighted-average common shares outstanding by approximately 6 million shares and (2) a reduction in the amount of annual preferred stock dividends paid by approximately $28 million when compared to the full year 2019 Outlook.

Full Year 2019 and 2020 Outlook

The current full year 2019 Outlook remains unchanged from the prior full year 2019 Outlook issued on July 17, 2019. The table below compares the midpoint of the full year 2020 Outlook and the midpoint of the full year 2019 Outlook for select metrics.

| (in millions) | Midpoint of Current Full Year 2020 Outlook |

Midpoint of Current Full Year 2019 Outlook |

Change | % Change | ||||

| Site rental revenues | $5,219 | $4,965 | +$254 | +5% | ||||

| Net income (loss) | $1,128 | $926 | +$202 | +22% | ||||

| Net income (loss) per share—diluted(a)(b) | $2.53 | $1.95 | +$0.58 | +30% | ||||

| Adjusted EBITDA(c) | $3,592 | $3,408 | +$184 | +5% | ||||

| AFFO(a)(c) | $2,685 | $2,479 | +$206 | +8% | ||||

| AFFO per share(a)(b)(c) | $6.33 | $5.94 | +$0.39 | +7% | ||||

| Weighted-average common shares outstanding – diluted(b) | 424 | 418 | +6 | +1% | ||||

(a) Attributable to CCIC common stockholders.

(b) The assumption for diluted weighted-average common shares outstanding for full year 2019 Outlook is based on the diluted common shares outstanding as of September 30, 2019, and does not include any assumed conversion of preferred stock in the share count. The full year 2020 Outlook is inclusive of the assumed conversion of preferred stock in August 2020, which we expect to result in (1) an increase in the diluted weighted-average common shares outstanding by approximately 6 million shares and (2) a reduction in the amount of annual preferred stock dividends paid by approximately $28 million when compared to the full year 2019 Outlook.

(c) See reconciliation of this non-GAAP financial measure to net income (loss) and definition included herein.

- The full year 2020 Outlook assumes the proposed merger between T-Mobile and Sprint closes prior to the end of the first quarter 2020.

- The 2020 Outlook also reflects the impact of the assumed conversion of preferred stock in August 2020. This conversion will increase the diluted weighted average common shares outstanding for 2020 by approximately 6 million and reduce the annual preferred stock dividends paid by approximately $28 million when compared to 2019.

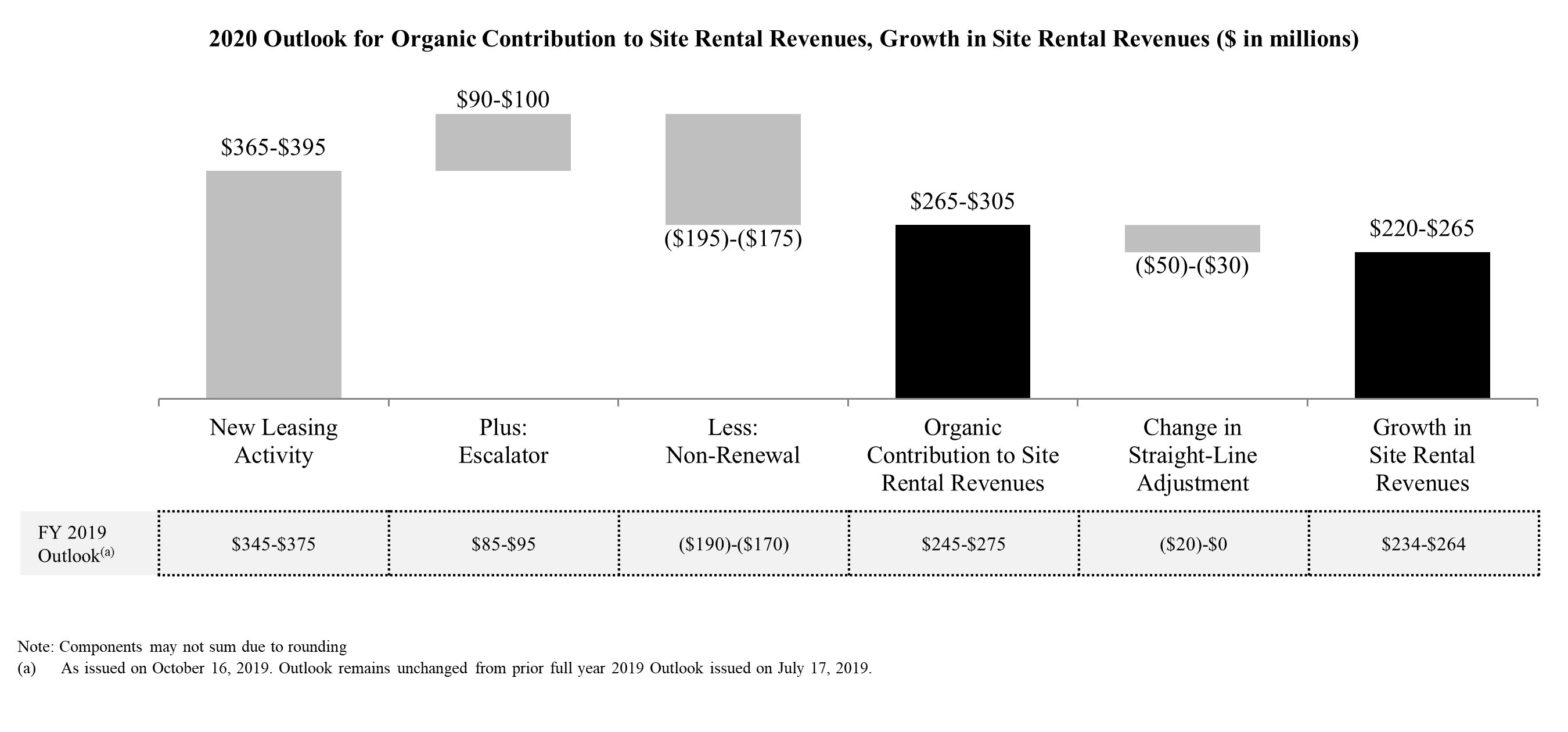

- The chart below reconciles the components of expected growth in site rental revenues from 2019 to 2020 of $220 million to $265 million, inclusive of expected Organic Contribution to Site Rental Revenues during 2020 of $265 million to $305 million.

Chart 1: https://www.globenewswire.com/NewsRoom/AttachmentNg/2ce1289e-1d70-4c18-9d2f-e1dd0f737671 - New leasing activity is expected to contribute $365 million to $395 million to 2020 Organic Contribution to Site Rental Revenues, consisting of new leasing activity from towers of $140 million to $150 million (compares to $135 million to $145 million for 2019), small cells of $65 million to $75 million (consistent with 2019 activity), and fiber solutions of $160 million to $170 million (compares to $145 million to $155 million for 2019).

- The Outlook also reflects an expected deployment of approximately 10,000 small cell nodes during 2020 (similar to expected deployment levels in 2019) and a consistent contribution to growth from fiber solutions when compared to 2019.

- The chart below reconciles the components of expected growth in AFFO from 2019 to 2020 of $185 million to $230 million.

Chart 2: https://www.globenewswire.com/NewsRoom/AttachmentNg/fb068b50-43cd-4b12-9f45-6f0a80798376 - Additional information is available in Crown Castle’s quarterly Supplemental Information Package posted in the Investors section of its website.

DIVIDEND INCREASE ANNOUNCEMENT

Crown Castle’s Board of Directors has declared a quarterly cash dividend of $1.20 per common share, representing an increase of approximately 7% over the previous quarterly dividend of $1.125 per share. The quarterly dividend will be payable on December 31, 2019 to common stockholders of record at the close of business on December 13, 2019. Future dividends are subject to the approval of Crown Castle’s Board of Directors.

CONFERENCE CALL DETAILS

Crown Castle has scheduled a conference call for Thursday, October 17, 2019, at 10:30 a.m. Eastern time to discuss its third quarter 2019 results. The conference call may be accessed by dialing 800-367-2403 and asking for the Crown Castle call (access code 2038078) at least 30 minutes prior to the start time. The conference call may also be accessed live over the Internet at investor.crowncastle.com. Supplemental materials for the call have been posted on the Crown Castle website at investor.crowncastle.com.

A telephonic replay of the conference call will be available from 1:30 p.m. Eastern time on Thursday, October 17, 2019, through 1:30 p.m. Eastern time on Wednesday, January 15, 2020, and may be accessed by dialing 888-203-1112 and using access code 2038078. An audio archive will also be available on the company’s website at investor.crowncastle.com shortly after the call and will be accessible for approximately 90 days.

ABOUT CROWN CASTLE

Crown Castle owns, operates and leases more than 40,000 cell towers and more than 75,000 route miles of fiber supporting small cells and fiber solutions across every major U.S. market. This nationwide portfolio of communications infrastructure connects cities and communities to essential data, technology and wireless service – bringing information, ideas and innovations to the people and businesses that need them. For more information on Crown Castle, please visit www.crowncastle.com.

Non-GAAP Financial Measures, Segment Measures and Other Calculations

This press release includes presentations of Adjusted EBITDA, Adjusted Funds from Operations (“AFFO”), including per share amounts, Funds from Operations (“FFO”), including per share amounts, and Organic Contribution to Site Rental Revenues, which are non-GAAP financial measures. These non-GAAP financial measures are not intended as alternative measures of operating results or cash flow from operations (as determined in accordance with Generally Accepted Accounting Principles (“GAAP”)).

Our non-GAAP financial measures may not be comparable to similarly titled measures of other companies, including other companies in the communications infrastructure sector or other real estate investment trusts (“REITs”). Our definition of FFO is consistent with guidelines from the National Association of Real Estate Investment Trusts with the exception of the impact of income taxes in periods prior to our REIT conversion in 2014.

In addition to the non-GAAP financial measures used herein, we also provide Segment Site Rental Gross Margin, Segment Services and Other Gross Margin and Segment Operating Profit, which are key measures used by management to evaluate our operating segments. These segment measures are provided pursuant to GAAP requirements related to segment reporting. In addition, we provide the components of certain GAAP measures, such as capital expenditures.

Our non-GAAP financial measures are presented as additional information because management believes these measures are useful indicators of the financial performance of our business. Among other things, management believes that:

- Adjusted EBITDA is useful to investors or other interested parties in evaluating our financial performance. Adjusted EBITDA is the primary measure used by management (1) to evaluate the economic productivity of our operations and (2) for purposes of making decisions about allocating resources to, and assessing the performance of, our operations. Management believes that Adjusted EBITDA helps investors or other interested parties meaningfully evaluate and compare the results of our operations (1) from period to period and (2) to our competitors, by removing the impact of our capital structure (primarily interest charges from our outstanding debt) and asset base (primarily depreciation, amortization and accretion) from our financial results. Management also believes Adjusted EBITDA is frequently used by investors or other interested parties in the evaluation of the communications infrastructure sector and other REITs to measure financial performance without regard to items such as depreciation, amortization and accretion which can vary depending upon accounting methods and the book value of assets. In addition, Adjusted EBITDA is similar to the measure of current financial performance generally used in our debt covenant calculations. Adjusted EBITDA should be considered only as a supplement to net income computed in accordance with GAAP as a measure of our performance.

- AFFO, including per share amounts, is useful to investors or other interested parties in evaluating our financial performance. Management believes that AFFO helps investors or other interested parties meaningfully evaluate our financial performance as it includes (1) the impact of our capital structure (primarily interest expense on our outstanding debt and dividends on our preferred stock) and (2) sustaining capital expenditures, and excludes the impact of our (a) asset base (primarily depreciation, amortization and accretion) and (b) certain non-cash items, including straight-lined revenues and expenses related to fixed escalations and rent free periods. GAAP requires rental revenues and expenses related to leases that contain specified rental increases over the life of the lease to be recognized evenly over the life of the lease. In accordance with GAAP, if payment terms call for fixed escalations, or rent free periods, the revenue or expense is recognized on a straight-lined basis over the fixed, non-cancelable term of the contract. Management notes that Crown Castle uses AFFO only as a performance measure. AFFO should be considered only as a supplement to net income computed in accordance with GAAP as a measure of our performance and should not be considered as an alternative to cash flows from operations or as residual cash flow available for discretionary investment.

- FFO, including per share amounts, is useful to investors or other interested parties in evaluating our financial performance. Management believes that FFO may be used by investors or other interested parties as a basis to compare our financial performance with that of other REITs. FFO helps investors or other interested parties meaningfully evaluate financial performance by excluding the impact of our asset base (primarily depreciation, amortization and accretion). FFO is not a key performance indicator used by Crown Castle. FFO should be considered only as a supplement to net income computed in accordance with GAAP as a measure of our performance and should not be considered as an alternative to cash flow from operations.

- Organic Contribution to Site Rental Revenues is useful to investors or other interested parties in understanding the components of the year-over-year changes in our site rental revenues computed in accordance with GAAP. Management uses the Organic Contribution to Site Rental Revenues to assess year-over-year growth rates for our rental activities, to evaluate current performance, to capture trends in rental rates, new leasing activities and tenant non-renewals in our core business, as well to forecast future results. Organic Contribution to Site Rental Revenues is not meant as an alternative measure of revenue and should be considered only as a supplement in understanding and assessing the performance of our site rental revenues computed in accordance with GAAP.

We define our non-GAAP financial measures, segment measures and other calculations as follows:

Non-GAAP Financial Measures

Adjusted EBITDA. We define Adjusted EBITDA as net income (loss) plus restructuring charges (credits), asset write-down charges, acquisition and integration costs, depreciation, amortization and accretion, amortization of prepaid lease purchase price adjustments, interest expense and amortization of deferred financing costs, (gains) losses on retirement of long-term obligations, net (gain) loss on interest rate swaps, (gains) losses on foreign currency swaps, impairment of available-for-sale securities, interest income, other (income) expense, (benefit) provision for income taxes, cumulative effect of a change in accounting principle, (income) loss from discontinued operations and stock-based compensation expense.

Adjusted Funds from Operations. We define Adjusted Funds from Operations as FFO before straight-lined revenue, straight-lined expense, stock-based compensation expense, non-cash portion of tax provision, non-real estate related depreciation, amortization and accretion, amortization of non-cash interest expense, other (income) expense, (gains) losses on retirement of long-term obligations, net (gain) loss on interest rate swaps, (gains) losses on foreign currency swaps, acquisition and integration costs, and adjustments for noncontrolling interests, and less sustaining capital expenditures.

AFFO per share. We define AFFO per share as AFFO divided by diluted weighted-average common shares outstanding.

Funds from Operations. We define Funds from Operations as net income plus real estate related depreciation, amortization and accretion and asset write-down charges, less noncontrolling interest and cash paid for preferred stock dividends, and is a measure of funds from operations attributable to CCIC common stockholders.

FFO per share. We define FFO per share as FFO divided by the diluted weighted-average common shares outstanding.

Organic Contribution to Site Rental Revenues. We define the Organic Contribution to Site Rental Revenues as the sum of the change in GAAP site rental revenues related to (1) new leasing activity, including revenues from the construction of small cells and the impact of prepaid rent, (2) escalators and less (3) non-renewals of tenant contracts.

Segment Measures

Segment Site Rental Gross Margin. We define Segment Site Rental Gross Margin as segment site rental revenues less segment site rental cost of operations, excluding stock-based compensation expense and prepaid lease purchase price adjustments recorded in consolidated site rental cost of operations.

Segment Services and Other Gross Margin. We define Segment Services and Other Gross Margin as segment services and other revenues less segment services and other cost of operations, excluding stock-based compensation expense recorded in consolidated services and other cost of operations.

Segment Operating Profit. We define Segment Operating Profit as segment site rental gross margin plus segment services and other gross margin, less selling, general and administrative expenses attributable to the respective segment.

All of these measurements of profit or loss are exclusive of depreciation, amortization and accretion, which are shown separately. Additionally, certain costs are shared across segments and are reflected in our segment measures through allocations that management believes to be reasonable.

Other Calculations

Discretionary capital expenditures. We define discretionary capital expenditures as those capital expenditures made with respect to activities which we believe exhibit sufficient potential to enhance long-term stockholder value. They primarily consist of expansion or development of communications infrastructure (including capital expenditures related to (1) enhancing communications infrastructure assets in order to add new tenants for the first time or support subsequent tenant equipment augmentations, or (2) modifying the structure of a communications infrastructure asset to accommodate additional tenants), and construction of new communications infrastructure. Discretionary capital expenditures also include purchases of land interests (which primarily relate to land assets under towers as we seek to manage our interests in the land beneath our towers), certain technology-related investments necessary to support and scale future customer demand for our communications infrastructure and other capital projects.

Integration capital expenditures. We define integration capital expenditures as those capital expenditures made as a result of integrating acquired companies into our business.

Sustaining capital expenditures. We define sustaining capital expenditures as those capital expenditures not otherwise categorized as either discretionary or integration capital expenditures, such as (1) maintenance capital expenditures on our communications infrastructure assets that enable our tenants’ ongoing quiet enjoyment of the communications infrastructure and (2) ordinary corporate capital expenditures.

The tables set forth on the following pages reconcile the non-GAAP financial measures used herein to comparable GAAP financial measures. The components in these tables may not sum to the total due to rounding.

Reconciliations of Non-GAAP Financial Measures, Segment Measures and Other Calculations to Comparable GAAP Financial Measures:

Reconciliation of Historical Adjusted EBITDA:

| For the Three Months Ended | For the Twelve Months Ended | ||||||||||

| September 30, 2019 | September 30, 2018 | December 31, 2018 | |||||||||

| (in millions) | |||||||||||

| Net income (loss) | $ | 272 | $ | 164 | $ | 671 | |||||

| Adjustments to increase (decrease) net income (loss): | |||||||||||

| Asset write-down charges | 2 | 8 | 26 | ||||||||

| Acquisition and integration costs | 4 | 4 | 27 | ||||||||

| Depreciation, amortization and accretion | 389 | 385 | 1,528 | ||||||||

| Amortization of prepaid lease purchase price adjustments | 5 | 5 | 20 | ||||||||

| Interest expense and amortization of deferred financing costs(a) | 173 | 160 | 642 | ||||||||

| (Gains) losses on retirement of long-term obligations | — | 32 | 106 | ||||||||

| Interest income | (2 | ) | (1 | ) | (5 | ) | |||||

| Other (income) expense | 5 | (1 | ) | (1 | ) | ||||||

| (Benefit) provision for income taxes | 5 | 5 | 19 | ||||||||

| Stock-based compensation expense | 29 | 32 | 108 | ||||||||

| Adjusted EBITDA(b)(c) | $ | 882 | $ | 793 | $ | 3,141 | |||||

(a) See the reconciliation of “components of historical interest expense and amortization of deferred financing costs” herein for a discussion of non-cash interest expense.

(b) See “Non-GAAP Financial Measures, Segment Measures and Other Calculations” herein for a discussion of our definition of Adjusted EBITDA.

(c) The above reconciliation excludes line items included in our definition which are not applicable for the periods shown.

Reconciliation of Current Outlook for Adjusted EBITDA:

| Full Year 2019 | Full Year 2020 | ||||||||||||||

| (in millions) | Outlook | Outlook | |||||||||||||

| Net income (loss) | $ | 896 | to | $ | 956 | $ | 1,088 | to | $ | 1,168 | |||||

| Adjustments to increase (decrease) net income (loss): | |||||||||||||||

| Asset write-down charges | $ | 23 | to | $ | 33 | $ | 20 | to | $ | 30 | |||||

| Acquisition and integration costs | $ | 11 | to | $ | 21 | $ | 7 | to | $ | 17 | |||||

| Depreciation, amortization and accretion | $ | 1,576 | to | $ | 1,611 | $ | 1,503 | to | $ | 1,598 | |||||

| Amortization of prepaid lease purchase price adjustments | $ | 19 | to | $ | 21 | $ | 18 | to | $ | 20 | |||||

| Interest expense and amortization of deferred financing costs(a) | $ | 674 | to | $ | 704 | $ | 691 | to | $ | 736 | |||||

| (Gains) losses on retirement of long-term obligations | $ | 2 | to | $ | 2 | $ | 0 | to | $ | 0 | |||||

| Interest income | $ | (8 | ) | to | $ | (4 | ) | $ | (7 | ) | to | $ | (3 | ) | |

| Other (income) expense | $ | 2 | to | $ | 4 | $ | (1 | ) | to | $ | 1 | ||||

| (Benefit) provision for income taxes | $ | 16 | to | $ | 24 | $ | 16 | to | $ | 24 | |||||

| Stock-based compensation expense | $ | 112 | to | $ | 120 | $ | 126 | to | $ | 130 | |||||

| Adjusted EBITDA(b)(c) | $ | 3,393 | to | $ | 3,423 | $ | 3,569 | to | $ | 3,614 | |||||

(a) See the reconciliation of “components of current outlook for interest expense and amortization of deferred financing costs” herein for a discussion of non-cash interest expense.

(b) See “Non-GAAP Financial Measures, Segment Measures and Other Calculations” herein for a discussion of our definition of Adjusted EBITDA.

(c) The above reconciliation excludes line items included in our definition which are not applicable for the periods shown.

Reconciliation of Historical FFO and AFFO:

| For the Three Months Ended | For the Nine Months Ended | For the Twelve Months Ended | |||||||||||||||||

| (in millions) | September 30, 2019 | September 30, 2018 | September 30, 2019 | September 30, 2018 | December 31, 2018 | ||||||||||||||

| Net income (loss) | $ | 272 | $ | 164 | $ | 729 | $ | 458 | $ | 671 | |||||||||

| Real estate related depreciation, amortization and accretion | 375 | 371 | 1,134 | 1,097 | 1,472 | ||||||||||||||

| Asset write-down charges | 2 | 8 | 13 | 18 | 26 | ||||||||||||||

| Dividends on preferred stock | (28 | ) | (28 | ) | (85 | ) | (85 | ) | (113 | ) | |||||||||

| FFO(a)(b)(c)(d) | $ | 622 | $ | 515 | $ | 1,789 | $ | 1,487 | $ | 2,055 | |||||||||

| Weighted-average common shares outstanding—diluted(e) | 418 | 416 | 418 | 414 | 415 | ||||||||||||||

| FFO per share(a)(b)(c)(d)(e) | $ | 1.49 | $ | 1.24 | $ | 4.28 | $ | 3.59 | $ | 4.95 | |||||||||

| FFO (from above) | $ | 622 | $ | 515 | $ | 1,789 | $ | 1,487 | $ | 2,055 | |||||||||

| Adjustments to increase (decrease) FFO: | |||||||||||||||||||

| Straight-lined revenue | (22 | ) | (17 | ) | (62 | ) | (53 | ) | (72 | ) | |||||||||

| Straight-lined expense | 24 | 23 | 70 | 69 | 90 | ||||||||||||||

| Stock-based compensation expense | 29 | 32 | 90 | 84 | 108 | ||||||||||||||

| Non-cash portion of tax provision | 1 | 2 | 2 | (1 | ) | 2 | |||||||||||||

| Non-real estate related depreciation, amortization and accretion | 14 | 14 | 42 | 41 | 56 | ||||||||||||||

| Amortization of non-cash interest expense | — | 2 | 1 | 5 | 7 | ||||||||||||||

| Other (income) expense | 5 | (1 | ) | 6 | — | (1 | ) | ||||||||||||

| (Gains) losses on retirement of long-term obligations | — | 32 | 2 | 106 | 106 | ||||||||||||||

| Acquisition and integration costs | 4 | 4 | 10 | 18 | 27 | ||||||||||||||

| Sustaining capital expenditures | (29 | ) | (27 | ) | (80 | ) | (75 | ) | (105 | ) | |||||||||

| AFFO(a)(b)(c)(d) | $ | 646 | $ | 579 | $ | 1,871 | $ | 1,683 | $ | 2,274 | |||||||||

| Weighted-average common shares outstanding—diluted(e) | 418 | 416 | 418 | 414 | 415 | ||||||||||||||

| AFFO per share(a)(b)(c)(d)(e) | $ | 1.55 | $ | 1.39 | $ | 4.48 | $ | 4.06 | $ | 5.48 | |||||||||

(a) See “Non-GAAP Financial Measures, Segment Measures and Other Calculations” herein for a discussion of our definitions of FFO, including per share amounts, and AFFO, including per share amounts.

(b) FFO and AFFO are reduced by cash paid for preferred stock dividends during the period in which they are paid.

(c) Attributable to CCIC common stockholders.

(d) The above reconciliation excludes line items included in our definition which are not applicable for the periods shown.

(e) For all periods presented, the diluted weighted-average common shares outstanding does not include any assumed conversion of preferred stock in the share count.

Reconciliation of Current Outlook for FFO and AFFO:

| Full Year 2019 | Full Year 2020 | |||||||||||||

| (in millions) | Outlook | Outlook | ||||||||||||

| Net income (loss) | $ | 896 | to | $ | 956 | $ | 1,088 | to | $ | 1,168 | ||||

| Real estate related depreciation, amortization and accretion | $ | 1,528 | to | $ | 1,548 | $ | 1,454 | to | $ | 1,534 | ||||

| Asset write-down charges | $ | 23 | to | $ | 33 | $ | 20 | to | $ | 30 | ||||

| Dividends on preferred stock | $ | (113 | ) | to | $ | (113 | ) | $ | (85 | ) | to | $ | (85 | ) |

| FFO(a)(b)(c)(d) | $ | 2,363 | to | $ | 2,393 | $ | 2,539 | to | $ | 2,584 | ||||

| Weighted-average common shares outstanding—diluted(e) | 418 | 424 | ||||||||||||

| FFO per share(a)(b)(c)(d)(e) | $ | 5.66 | to | $ | 5.73 | $ | 5.99 | to | $ | 6.09 | ||||

| FFO (from above) | $ | 2,363 | to | $ | 2,393 | $ | 2,539 | to | $ | 2,584 | ||||

| Adjustments to increase (decrease) FFO: | ||||||||||||||

| Straight-lined revenue | $ | (74 | ) | to | $ | (54 | ) | $ | (53 | ) | to | $ | (33 | ) |

| Straight-lined expense | $ | 81 | to | $ | 101 | $ | 70 | to | $ | 90 | ||||

| Stock-based compensation expense | $ | 112 | to | $ | 120 | $ | 126 | to | $ | 130 | ||||

| Non-cash portion of tax provision | $ | (6 | ) | to | $ | 9 | $ | (6 | ) | to | $ | 9 | ||

| Non-real estate related depreciation, amortization and accretion | $ | 48 | to | $ | 63 | $ | 49 | to | $ | 64 | ||||

| Amortization of non-cash interest expense | $ | (5 | ) | to | $ | 5 | $ | (4 | ) | to | $ | 6 | ||

| Other (income) expense | $ | 2 | to | $ | 4 | $ | (1 | ) | to | $ | 1 | |||

| (Gains) losses on retirement of long-term obligations | $ | 2 | to | $ | 2 | $ | 0 | to | $ | 0 | ||||

| Acquisition and integration costs | $ | 11 | to | $ | 21 | $ | 7 | to | $ | 17 | ||||

| Sustaining capital expenditures | $ | (136 | ) | to | $ | (106 | ) | $ | (123 | ) | to | $ | (103 | ) |

| AFFO(a)(b)(c)(d) | $ | 2,464 | to | $ | 2,494 | $ | 2,662 | to | $ | 2,707 | ||||

| Weighted-average common shares outstanding—diluted(e) | 418 | 424 | ||||||||||||

| AFFO per share(a)(b)(c)(d)(e) | $ | 5.90 | to | $ | 5.97 | $ | 6.28 | to | $ | 6.38 | ||||

(a) See “Non-GAAP Financial Measures, Segment Measures and Other Calculations” herein for a discussion of our definitions of FFO, including per share amounts, and AFFO, including per share amounts.

(b) FFO and AFFO are reduced by cash paid for preferred stock dividends during the period in which they are paid.

(c) Attributable to CCIC common stockholders.

(d) The above reconciliation excludes line items included in our definition which are not applicable for the periods shown.

(e) The assumption for diluted weighted-average common shares outstanding for full year 2019 Outlook is based on the diluted common shares outstanding as of September 30, 2019, and does not include any assumed conversion of preferred stock in the share count. The full year 2020 Outlook is inclusive of the assumed conversion of preferred stock in August 2020, which we expect to result in (1) an increase in the diluted weighted-average common shares outstanding by approximately 6 million shares and (2) a reduction in the amount of annual preferred stock dividends paid by approximately $28 million when compared to the full year 2019 Outlook.

For Comparative Purposes – Reconciliation of Previous Outlook for Adjusted EBITDA:

| Previously Issued | |||||||

| Full Year 2019 | |||||||

| (in millions) | Outlook | ||||||

| Net income (loss) | $ | 896 | to | $ | 956 | ||

| Adjustments to increase (decrease) net income (loss): | |||||||

| Asset write-down charges | $ | 23 | to | $ | 33 | ||

| Acquisition and integration costs | $ | 11 | to | $ | 21 | ||

| Depreciation, amortization and accretion | $ | 1,576 | to | $ | 1,611 | ||

| Amortization of prepaid lease purchase price adjustments | $ | 19 | to | $ | 21 | ||

| Interest expense and amortization of deferred financing costs | $ | 674 | to | $ | 704 | ||

| (Gains) losses on retirement of long-term obligations | $ | 2 | to | $ | 2 | ||

| Interest income | $ | (8 | ) | to | $ | (4 | ) |

| Other (income) expense | $ | 2 | to | $ | 4 | ||

| (Benefit) provision for income taxes | $ | 16 | to | $ | 24 | ||

| Stock-based compensation expense | $ | 112 | to | $ | 120 | ||

| Adjusted EBITDA(a)(b) | $ | 3,393 | to | $ | 3,423 | ||

(a) See “Non-GAAP Financial Measures, Segment Measures and Other Calculations” herein for a discussion of our definition of Adjusted EBITDA.

(b) The above reconciliation excludes line items included in our definition which are not applicable for the periods shown.

For Comparative Purposes – Reconciliation of Previous Outlook for FFO and AFFO:

| Previously Issued | |||||||

| Full Year 2019 | |||||||

| (in millions) | Outlook | ||||||

| Net income (loss) | $ | 896 | to | $ | 956 | ||

| Real estate related depreciation, amortization and accretion | $ | 1,528 | to | $ | 1,548 | ||

| Asset write-down charges | $ | 23 | to | $ | 33 | ||

| Dividends on preferred stock | $ | (113 | ) | to | $ | (113 | ) |

| FFO(a)(b)(c)(d) | $ | 2,363 | to | $ | 2,393 | ||

| Weighted-average common shares outstanding—diluted(e) | 418 | ||||||

| FFO per share(a)(b)(c)(d)(e) | $ | 5.66 | to | $ | 5.73 | ||

| FFO (from above) | $ | 2,363 | to | $ | 2,393 | ||

| Adjustments to increase (decrease) FFO: | |||||||

| Straight-lined revenue | $ | (74 | ) | to | $ | (54 | ) |

| Straight-lined expense | $ | 81 | to | $ | 101 | ||

| Stock-based compensation expense | $ | 112 | to | $ | 120 | ||

| Non-cash portion of tax provision | $ | (6 | ) | to | $ | 9 | |

| Non-real estate related depreciation, amortization and accretion | $ | 48 | to | $ | 63 | ||

| Amortization of non-cash interest expense | $ | (5 | ) | to | $ | 5 | |

| Other (income) expense | $ | 2 | to | $ | 4 | ||

| (Gains) losses on retirement of long-term obligations | $ | 2 | to | $ | 2 | ||

| Acquisition and integration costs | $ | 11 | to | $ | 21 | ||

| Maintenance capital expenditures | $ | (90 | ) | to | $ | (75 | ) |

| Corporate capital expenditures | $ | (46 | ) | to | $ | (31 | ) |

| AFFO(a)(b)(c)(d) | $ | 2,464 | to | $ | 2,494 | ||

| Weighted-average common shares outstanding—diluted(e) | 418 | ||||||

| AFFO per share(a)(b)(c)(d)(e) | $ | 5.90 | to | $ | 5.97 | ||

(a) See “Non-GAAP Financial Measures, Segment Measures and Other Calculations” herein for a discussion of our definitions of FFO, including per share amounts, and AFFO, including per share amounts.

(b) FFO and AFFO are reduced by cash paid for preferred stock dividends during the period in which they are paid.

(c) Attributable to CCIC common stockholders.

(d) The above reconciliation excludes line items included in our definition which are not applicable for the periods shown.

(e) The diluted weighted-average common shares outstanding in the previously issued full year 2019 Outlook does not include any assumed conversion of preferred stock in the share count.

The components of changes in site rental revenues for the quarters ended September 30, 2019 and 2018 are as follows:

| Three Months Ended September 30, |

|||||||

| (dollars in millions) | 2019 | 2018 | |||||

| Components of changes in site rental revenues(a): | |||||||

| Prior year site rental revenues exclusive of straight-lined revenues associated with fixed escalators(b)(c) | $ | 1,168 | $ | 896 | |||

| New leasing activity(b)(c) | 92 | 54 | |||||

| Escalators | 22 | 21 | |||||

| Non-renewals | (44 | ) | (23 | ) | |||

| Organic Contribution to Site Rental Revenues(d) | 70 | 52 | |||||

| Straight-lined revenues associated with fixed escalators | 22 | 17 | |||||

| Acquisitions(e) | — | 219 | |||||

| Other | — | — | |||||

| Total GAAP site rental revenues | $ | 1,260 | $ | 1,184 | |||

| Year-over-year changes in revenue: | |||||||

| Reported GAAP site rental revenues | 6.4 | % | |||||

| Organic Contribution to Site Rental Revenues(d)(f) | 6.0 | % | |||||

(a) Additional information regarding Crown Castle’s site rental revenues, including projected revenue from tenant licenses, straight-lined revenues and prepaid rent is available in Crown Castle’s quarterly Supplemental Information Package posted in the Investors section of its website.

(b) Includes revenues from amortization of prepaid rent in accordance with GAAP.

(c) Includes revenues from the construction of new small cell nodes, exclusive of straight-lined revenues related to fixed escalators.

(d) See “Non-GAAP Financial Measures, Segment Measures and Other Calculations” herein.

(e) Represents the initial contribution of recent acquisitions. The financial impact of recent acquisitions is excluded from Organic Contribution to Site Rental Revenues until the one-year anniversary of the acquisition.

(f) Calculated as the percentage change from prior year site rental revenues, exclusive of straight-lined revenues associated with fixed escalations, compared to Organic Contribution to Site Rental Revenues for the current period.

The components of the changes in site rental revenues for the years ending December 31, 2019 and December 31, 2020 are forecasted as follows:

| (dollars in millions) | Full Year 2019 Outlook |

Full Year 2020 Outlook | ||||

| Components of changes in site rental revenues(a): | ||||||

| Prior year site rental revenues exclusive of straight-lined revenues associated with fixed escalators(b)(c) | $ | 4,643 | $ | 4,901 | ||

| New leasing activity(b)(c) | 345-375 | 365-395 | ||||

| Escalators | 85-95 | 90-100 | ||||

| Non-renewals | (190)-(170) | (195)-(175) | ||||

| Organic Contribution to Site Rental Revenues(d) | 245-275 | 265-305 | ||||

| Straight-lined revenues associated with fixed escalators | 54-74 | 33-53 | ||||

| Acquisitions(e) | — | — | ||||

| Other | — | — | ||||

| Total GAAP site rental revenues | $4,950-$4,980 | $5,196-$5,241 | ||||

| Year-over-year changes in revenue: | ||||||

| Reported GAAP site rental revenues(f) | 5.3 | % | 5.1 | % | ||

| Organic Contribution to Site Rental Revenues(d)(f)(g) | 5.6 | % | 5.8 | % | ||

(a) Additional information regarding Crown Castle’s site rental revenues, including projected revenue from tenant licenses, straight-lined revenues and prepaid rent is available in Crown Castle’s quarterly Supplemental Information Package posted in the Investors section of its website.

(b) Includes revenues from amortization of prepaid rent in accordance with GAAP.

(c) Includes revenues from the construction of new small cell nodes, exclusive of straight-lined revenues related to fixed escalators.

(d) See “Non-GAAP Financial Measures, Segment Measures and Other Calculations” herein.

(e) Represents the contribution from recent acquisitions. The financial impact of recent acquisitions is excluded from Organic Contribution to Site Rental Revenues until the one-year anniversary of the acquisition.

(f) Calculated based on midpoint of full year 2019 Outlook and full year 2020 Outlook.

(g) Calculated as the percentage change from prior year site rental revenues, exclusive of straight-lined revenues associated with fixed escalations, compared to Organic Contribution to Site Rental Revenues for the current period.

Components of Historical Interest Expense and Amortization of Deferred Financing Costs:

| For the Three Months Ended | |||||||

| (in millions) | September 30, 2019 | September 30, 2018 | |||||

| Interest expense on debt obligations | $ | 173 | $ | 158 | |||

| Amortization of deferred financing costs and adjustments on long-term debt, net | 5 | 5 | |||||

| Other, net | (5 | ) | (3 | ) | |||

| Interest expense and amortization of deferred financing costs | $ | 173 | $ | 160 | |||

Components of Current Outlook for Interest Expense and Amortization of Deferred Financing Costs:

| Full Year 2019 | Full Year 2020 | ||||||||||||||

| (in millions) | Outlook | Outlook | |||||||||||||

| Interest expense on debt obligations | $ | 683 | to | $ | 693 | $ | 703 | to | $ | 723 | |||||

| Amortization of deferred financing costs and adjustments on long-term debt, net | $ | 17 | to | $ | 22 | $ | 20 | to | $ | 25 | |||||

| Other, net | $ | (22 | ) | to | $ | (17 | ) | $ | (24 | ) | to | $ | (19 | ) | |

| Interest expense and amortization of deferred financing costs | $ | 674 | to | $ | 704 | $ | 691 | to | $ | 736 | |||||

Debt balances and maturity dates as of September 30, 2019 are as follows:

| (in millions) | Face Value | Final Maturity | ||

| Cash, cash equivalents and restricted cash | $ | 325 | ||

| 3.849% Secured Notes | 1,000 | Apr. 2023 | ||

| Secured Notes, Series 2009-1, Class A-2(a) | 69 | Aug. 2029 | ||

| Tower Revenue Notes, Series 2015-1(b) | 300 | May 2042 | ||

| Tower Revenue Notes, Series 2018-1(b) | 250 | July 2043 | ||

| Tower Revenue Notes, Series 2015-2(b) | 700 | May 2045 | ||

| Tower Revenue Notes, Series 2018-2(b) | 750 | July 2048 | ||

| Finance leases and other obligations | 233 | Various | ||

| Total secured debt | $ | 3,302 | ||

| 2016 Revolver | 390 | June 2024 | ||

| 2016 Term Loan A | 2,326 | June 2024 | ||

| 2019 Commercial Paper Notes(c) | 0 | N/A | ||

| 3.400% Senior Notes | 850 | Feb. 2021 | ||

| 2.250% Senior Notes | 700 | Sept. 2021 | ||

| 4.875% Senior Notes | 850 | Apr. 2022 | ||

| 5.250% Senior Notes | 1,650 | Jan. 2023 | ||

| 3.150% Senior Notes | 750 | July 2023 | ||

| 3.200% Senior Notes | 750 | Sept. 2024 | ||

| 4.450% Senior Notes | 900 | Feb. 2026 | ||

| 3.700% Senior Notes | 750 | June 2026 | ||

| 4.000% Senior Notes | 500 | Mar. 2027 | ||

| 3.650% Senior Notes | 1,000 | Sept. 2027 | ||

| 3.800% Senior Notes | 1,000 | Feb. 2028 | ||

| 4.300% Senior Notes | 600 | Feb. 2029 | ||

| 3.100% Senior Notes | 550 | Nov. 2029 | ||

| 4.750% Senior Notes | 350 | May 2047 | ||

| 5.200% Senior Notes | 400 | Feb. 2049 | ||

| 4.000% Senior Notes | 350 | Nov. 2049 | ||

| Total unsecured debt | $ | 14,666 | ||

| Total net debt | $ | 17,643 | ||

(a) The Senior Secured Notes, 2009-1, Class A-2 principal amortizes during the period beginning in September 2019 and ending in August 2029.

(b) The Senior Secured Tower Revenue Notes, Series 2015-1 and 2015-2 have anticipated repayment dates in 2022 and 2025, respectively. The Senior Secured Tower Revenue Notes, Series 2018-1 and 2018-2 have anticipated repayment dates in 2023 and 2028, respectively.

(c) As of September 30, 2019, there were no outstanding 2019 Commercial Paper Notes. The maturities of the 2019 Commercial Paper Notes, when outstanding, may vary but may not exceed 397 days from the date of issue.

Net Debt to Last Quarter Annualized Adjusted EBITDA is computed as follows:

| (dollars in millions) | For the Three Months Ended September 30, 2019 | ||

| Total face value of debt | $ | 17,968 | |

| Ending cash, cash equivalents and restricted cash | 325 | ||

| Total Net Debt | $ | 17,643 | |

| Adjusted EBITDA for the three months ended September 30, 2019 | $ | 882 | |

| Last quarter annualized Adjusted EBITDA | 3,528 | ||

| Net Debt to Last Quarter Annualized Adjusted EBITDA | 5.0 | x | |

Components of Capital Expenditures:

| For the Three Months Ended | |||||||||||||||||||||||||

| (in millions) | September 30, 2019 | September 30, 2018 | |||||||||||||||||||||||

| Towers | Fiber | Other | Total | Towers | Fiber | Other | Total | ||||||||||||||||||

| Discretionary: | |||||||||||||||||||||||||

| Purchases of land interests | $ | 18 | $ | — | $ | — | $ | 18 | $ | 14 | $ | — | $ | — | $ | 14 | |||||||||

| Communications infrastructure construction and improvements | 120 | 371 | — | 491 | 100 | 336 | — | 436 | |||||||||||||||||

| Sustaining | 8 | 11 | 10 | 29 | 9 | 12 | 5 | 27 | |||||||||||||||||

| Integration | — | — | 2 | 2 | — | — | 1 | 1 | |||||||||||||||||

| Total | $ | 146 | $ | 382 | $ | 12 | $ | 540 | $ | 123 | $ | 348 | $ | 7 | $ | 478 | |||||||||

Note: See “Non-GAAP Financial Measures, Segment Measures and Other Calculations” herein for further discussion of our components of capital expenditures.

Cautionary Language Regarding Forward-Looking Statements

This press release contains forward-looking statements and information that are based on our management’s current expectations. Such statements include our Outlook and plans, projections, and estimates regarding (1) potential benefits, growth, returns, opportunities and tenant and shareholder value which may be derived from our business, assets, investments, acquisitions and dividends, (2) our strategy, strategic position, business model and capabilities, the strength of our business and fundamentals of our business and industry, (3) our customers’ investment in network improvements and deployment of cell sites, spectrum and 5G, (4) our long-term prospects and the trends impacting our business (including growth in mobile data traffic), (5) the potential benefits and contributions which may be derived from our acquisitions, including the contribution to or impact on our financial or operating results, (6) leasing environment and activity, including growth thereof and the contribution to our financial or operating results therefrom, (7) our small cell deployment, (8) our investments in our business and the potential growth, returns and benefits therefrom, (9) our dividends (including timing of payment thereof) and our dividend (including on a per share basis) growth rate, including its driving factors, and targets, (10) our portfolio of assets, including demand therefor, strategic position thereof and opportunities created thereby, (11) assumed conversion of preferred stock and the impact therefrom, (12) the approval of the proposed merger between T-Mobile and Sprint and timing of the closing thereof, (13) contribution to growth from fiber solutions, (14) cash flows, including growth thereof, (15) tenant non-renewals, including the impact and timing thereof, (16) capital expenditures, including sustaining and discretionary capital expenditures, and the timing thereof, (17) straight-line adjustments, (18) site rental revenues and estimated growth thereof, (19) site rental cost of operations, (20) net income (including on a per share basis) and estimated growth thereof, (21) Adjusted EBITDA, including the impact of the timing of certain components thereof and estimated growth thereof, (22) expenses, including interest expense and amortization of deferred financing costs, (23) FFO (including on a per share basis) and estimated growth thereof, (24) AFFO (including on a per share basis) and estimated growth thereof and corresponding driving factors, (25) Organic Contribution to Site Rental Revenues, (26) our weighted-average common shares outstanding (including on a diluted basis) and estimated growth thereof, (27) services contribution, including the timing thereof, and (28) the utility of certain financial measures, including non-GAAP financial measures. Such forward-looking statements are subject to certain risks, uncertainties and assumptions prevailing market conditions and the following:

- Our business depends on the demand for our communications infrastructure, driven primarily by demand for data, and we may be adversely affected by any slowdown in such demand. Additionally, a reduction in the amount or change in the mix of network investment by our tenants may materially and adversely affect our business (including reducing demand for our communications infrastructure or services).

- A substantial portion of our revenues is derived from a small number of tenants, and the loss, consolidation or financial instability of any of such tenants may materially decrease revenues or reduce demand for our communications infrastructure and services.

- The expansion or development of our business, including through acquisitions, increased product offerings or other strategic growth opportunities, may cause disruptions in our business, which may have an adverse effect on our business, operations or financial results.

- Our Fiber segment has expanded rapidly, and the Fiber business model contains certain differences from our Towers business model, resulting in different operational risks. If we do not successfully operate our Fiber business model or identify or manage the related operational risks, such operations may produce results that are less than anticipated.

- Failure to timely and efficiently execute on our construction projects could adversely affect our business.

- Our substantial level of indebtedness could adversely affect our ability to react to changes in our business, and the terms of our debt instruments and our 6.875% Mandatory Convertible Preferred Stock limit our ability to take a number of actions that our management might otherwise believe to be in our best interests. In addition, if we fail to comply with our covenants, our debt could be accelerated.

- We have a substantial amount of indebtedness. In the event we do not repay or refinance such indebtedness, we could face substantial liquidity issues and might be required to issue equity securities or securities convertible into equity securities, or sell some of our assets to meet our debt payment obligations.

- Sales or issuances of a substantial number of shares of our common stock or securities convertible into shares of our common stock may adversely affect the market price of our common stock.

- As a result of competition in our industry, we may find it more difficult to negotiate favorable rates on our new or renewing tenant contracts.

- New technologies may reduce demand for our communications infrastructure or negatively impact our revenues.

- If we fail to retain rights to our communications infrastructure, including the land interests under our towers and the right-of-way and other agreements related to our small cells and fiber solutions, our business may be adversely affected.

- Our services business has historically experienced significant volatility in demand, which reduces the predictability of our results.

- New wireless technologies may not deploy or be adopted by tenants as rapidly or in the manner projected.

- If we fail to comply with laws or regulations which regulate our business and which may change at any time, we may be fined or even lose our right to conduct some of our business.

- If radio frequency emissions from wireless handsets or equipment on our communications infrastructure are demonstrated to cause negative health effects, potential future claims could adversely affect our operations, costs or revenues.

- Certain provisions of our restated certificate of incorporation, amended and restated by-laws and operative agreements, and domestic and international competition laws may make it more difficult for a third party to acquire control of us or for us to acquire control of a third party, even if such a change in control would be beneficial to our stockholders.

- We may be vulnerable to security breaches or other unforeseen events that could adversely affect our operations, business, and reputation.

- Future dividend payments to our stockholders will reduce the availability of our cash on hand available to fund future discretionary investments, and may result in a need to incur indebtedness or issue equity securities to fund growth opportunities. In such event, the then current economic, credit market or equity market conditions will impact the availability or cost of such financing, which may hinder our ability to grow our per share results of operations.

- Remaining qualified to be taxed as a REIT involves highly technical and complex provisions of the U.S. Internal Revenue Code. Failure to remain qualified as a REIT would result in our inability to deduct dividends to stockholders when computing our taxable income, which would reduce our available cash.

- If we fail to pay scheduled dividends on our 6.875% Mandatory Convertible Preferred Stock, in cash, common stock, or any combination of cash and common stock, we will be prohibited from paying dividends on our common stock, which may jeopardize our status as a REIT.

- Complying with REIT requirements, including the 90% distribution requirement, may limit our flexibility or cause us to forgo otherwise attractive opportunities, including certain discretionary investments and potential financing alternatives.

- REIT related ownership limitations and transfer restrictions may prevent or restrict certain transfers of our capital stock.

Should one or more of these or other risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those expected. More information about potential risk factors which could affect our results is included in our filings with the SEC. Our filings with the SEC are available through the SEC website at www.sec.gov or through our investor relations website at investor.crowncastle.com. We use our investor relations website to disclose information about us that may be deemed to be material. We encourage investors, the media and others interested in us to visit our investor relations website from time to time to review up-to-date information or to sign up for e-mail alerts to be notified when new or updated information is posted on the site.

As used in this release, the term “including,” and any variation thereof, means “including without limitation.”

CROWN CASTLE INTERNATIONAL CORP.

CONDENSED CONSOLIDATED BALANCE SHEET (UNAUDITED)

(Amounts in millions, except par values)

| September 30, 2019 |

December 31, 2018 |

||||||

| ASSETS | |||||||

| Current assets: | |||||||

| Cash and cash equivalents | $ | 182 | $ | 277 | |||

| Restricted cash | 138 | 131 | |||||

| Receivables, net | 667 | 501 | |||||

| Prepaid expenses(a) | 99 | 172 | |||||

| Other current assets | 167 | 148 | |||||

| Total current assets | 1,253 | 1,229 | |||||

| Deferred site rental receivables | 1,413 | 1,366 | |||||

| Property and equipment, net | 14,416 | 13,676 | |||||

| Operating lease right-of-use assets(a) | 6,112 | — | |||||

| Goodwill | 10,078 | 10,078 | |||||

| Other intangible assets, net(a) | 4,968 | 5,516 | |||||

| Long-term prepaid rent and other assets, net(a) | 104 | 920 | |||||

| Total assets | $ | 38,344 | $ | 32,785 | |||

| LIABILITIES AND EQUITY | |||||||

| Current liabilities: | |||||||

| Accounts payable | $ | 368 | $ | 313 | |||

| Accrued interest | 110 | 148 | |||||

| Deferred revenues | 525 | 498 | |||||

| Other accrued liabilities(a) | 335 | 351 | |||||

| Current maturities of debt and other obligations | 100 | 107 | |||||

| Current portion of operating lease liabilities(a) | 296 | — | |||||

| Total current liabilities | 1,734 | 1,417 | |||||

| Debt and other long-term obligations | 17,750 | 16,575 | |||||

| Operating lease liabilities(a) | 5,480 | — | |||||

| Other long-term liabilities(a) | 2,055 | 2,759 | |||||

| Total liabilities | 27,019 | 20,751 | |||||

| Commitments and contingencies | |||||||

| CCIC stockholders’ equity: | |||||||

| Common stock, $0.01 par value; 600 shares authorized; shares issued and outstanding: September 30, 2019—416 and December 31, 2018—415 | 4 | 4 | |||||

| 6.875% Mandatory Convertible Preferred Stock, Series A, $0.01 par value; 20 shares authorized; shares issued and outstanding: September 30, 2019—2 and December 31, 2018—2; aggregate liquidation value: September 30, 2019—$1,650 and December 31, 2018—$1,650 | — | — | |||||

| Additional paid-in capital | 17,829 | 17,767 | |||||

| Accumulated other comprehensive income (loss) | (5 | ) | (5 | ) | |||

| Dividends/distributions in excess of earnings | (6,503 | ) | (5,732 | ) | |||

| Total equity | 11,325 | 12,034 | |||||

| Total liabilities and equity | $ | 38,344 | $ | 32,785 | |||

(a) Effective January 1, 2019, we adopted new guidance on the recognition, measurement, presentation and disclosure of leases. The new guidance requires lessees to recognize a lease liability, initially measured at the present value of the lease payments for all leases, and a corresponding right-of-use asset. The accounting for lessors remained largely unchanged from previous guidance. As a result of the new guidance for leases, on the effective date, certain amounts related to our lessee arrangements that were previously reported separately have been de-recognized and reclassified into “Operating lease right-of-use assets” on the condensed consolidated balance sheet as of September 30, 2019.

CROWN CASTLE INTERNATIONAL CORP.

CONDENSED CONSOLIDATED STATEMENT OF OPERATIONS (UNAUDITED)

(Amounts in millions, except per share amounts)

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

| 2019 | 2018 | 2019 | 2018 | ||||||||||||

| Net revenues: | |||||||||||||||

| Site rental | $ | 1,260 | $ | 1,184 | $ | 3,718 | $ | 3,507 | |||||||

| Services and other | 254 | 191 | 700 | 497 | |||||||||||

| Net revenues | 1,514 | 1,375 | 4,418 | 4,004 | |||||||||||

| Operating expenses: | |||||||||||||||

| Costs of operations (exclusive of depreciation, amortization and accretion): | |||||||||||||||

| Site rental | 369 | 355 | 1,095 | 1,057 | |||||||||||

| Services and other | 147 | 119 | 410 | 304 | |||||||||||

| Selling, general and administrative | 150 | 145 | 457 | 418 | |||||||||||

| Asset write-down charges | 2 | 8 | 13 | 18 | |||||||||||

| Acquisition and integration costs | 4 | 4 | 10 | 18 | |||||||||||

| Depreciation, amortization and accretion | 389 | 385 | 1,176 | 1,138 | |||||||||||

| Total operating expenses | 1,061 | 1,016 | 3,161 | 2,953 | |||||||||||

| Operating income (loss) | 453 | 359 | 1,257 | 1,051 | |||||||||||

| Interest expense and amortization of deferred financing costs | (173 | ) | (160 | ) | (510 | ) | (478 | ) | |||||||

| Gains (losses) on retirement of long-term obligations | — | (32 | ) | (2 | ) | (106 | ) | ||||||||

| Interest income | 2 | 1 | 5 | 4 | |||||||||||

| Other income (expense) | (5 | ) | 1 | (6 | ) | — | |||||||||

| Income (loss) before income taxes | 277 | 169 | 744 | 471 | |||||||||||

| Benefit (provision) for income taxes | (5 | ) | (5 | ) | (15 | ) | (13 | ) | |||||||

| Net income (loss) | 272 | 164 | 729 | 458 | |||||||||||

| Dividends on preferred stock | (28 | ) | (28 | ) | (85 | ) | (85 | ) | |||||||

| Net income (loss) attributable to CCIC common stockholders | $ | 244 | $ | 136 | $ | 644 | $ | 373 | |||||||

| Net income (loss) attributable to CCIC common stockholders, per common share: | |||||||||||||||

| Net income (loss) attributable to CCIC common stockholders, basic | $ | 0.59 | $ | 0.33 | $ | 1.55 | $ | 0.90 | |||||||

| Net income (loss) attributable to CCIC common stockholders, diluted | $ | 0.58 | $ | 0.33 | $ | 1.54 | $ | 0.90 | |||||||

| Weighted-average common shares outstanding: | |||||||||||||||

| Basic | 416 | 415 | 416 | 413 | |||||||||||

| Diluted | 418 | 416 | 418 | 414 | |||||||||||

CROWN CASTLE INTERNATIONAL CORP.

CONDENSED CONSOLIDATED STATEMENT OF CASH FLOWS (UNAUDITED)

(In millions of dollars)

| Nine Months Ended September 30, | |||||||

| 2019 | 2018 | ||||||

| Cash flows from operating activities: | |||||||

| Net income (loss) | $ | 729 | $ | 458 | |||

| Adjustments to reconcile net income (loss) to net cash provided by (used for) operating activities: | |||||||

| Depreciation, amortization and accretion | 1,176 | 1,138 | |||||

| (Gains) losses on retirement of long-term obligations | 2 | 106 | |||||

| Amortization of deferred financing costs and other non-cash interest | 1 | 5 | |||||

| Stock-based compensation expense | 91 | 79 | |||||

| Asset write-down charges | 13 | 18 | |||||

| Deferred income tax (benefit) provision | 2 | 2 | |||||

| Other non-cash adjustments, net | 4 | 2 | |||||

| Changes in assets and liabilities, excluding the effects of acquisitions: | |||||||

| Increase (decrease) in liabilities | 101 | 144 | |||||

| Decrease (increase) in assets | (228 | ) | (177 | ) | |||

| Net cash provided by (used for) operating activities | 1,891 | 1,775 | |||||

| Cash flows from investing activities: | |||||||

| Payments for acquisitions, net of cash acquired | (15 | ) | (26 | ) | |||

| Capital expenditures | (1,538 | ) | (1,241 | ) | |||

| Other investing activities, net | 3 | (14 | ) | ||||

| Net cash provided by (used for) investing activities | (1,550 | ) | (1,281 | ) | |||

| Cash flows from financing activities: | |||||||

| Proceeds from issuance of long-term debt | 1,895 | 2,743 | |||||

| Principal payments on debt and other long-term obligations | (59 | ) | (76 | ) | |||

| Purchases and redemptions of long-term debt | (12 | ) | (2,346 | ) | |||

| Borrowings under revolving credit facility | 1,585 | 1,290 | |||||

| Payments under revolving credit facility | (2,270 | ) | (1,465 | ) | |||

| Payments for financing costs | (24 | ) | (33 | ) | |||

| Net proceeds from issuance of common stock | — | 841 | |||||

| Purchases of common stock | (44 | ) | (34 | ) | |||

| Dividends/distributions paid on common stock | (1,415 | ) | (1,315 | ) | |||

| Dividends paid on preferred stock | (85 | ) | (85 | ) | |||

| Net cash provided by (used for) financing activities | (429 | ) | (480 | ) | |||

| Net increase (decrease) in cash, cash equivalents, and restricted cash | (88 | ) | 14 | ||||

| Effect of exchange rate changes on cash | — | (1 | ) | ||||

| Cash, cash equivalents, and restricted cash at beginning of period | 413 | 440 | |||||

| Cash, cash equivalents, and restricted cash at end of period | $ | 325 | $ | 453 | |||

| Supplemental disclosure of cash flow information: | |||||||

| Interest paid | 547 | 503 | |||||

| Income taxes paid | 13 | 15 | |||||

CROWN CASTLE INTERNATIONAL CORP.

SEGMENT OPERATING RESULTS (UNAUDITED)

(In millions of dollars)

| SEGMENT OPERATING RESULTS | |||||||||||||||||||||||||||||||

| Three Months Ended September 30, 2019 | Three Months Ended September 30, 2018 | ||||||||||||||||||||||||||||||

| Towers | Fiber | Other | Consolidated Total | Towers | Fiber | Other | Consolidated Total | ||||||||||||||||||||||||

| Segment site rental revenues | $ | 829 | $ | 431 | $ | 1,260 | $ | 782 | $ | 402 | $ | 1,184 | |||||||||||||||||||

| Segment services and other revenues | 250 | 4 | 254 | 189 | 2 | 191 | |||||||||||||||||||||||||

| Segment revenues | 1,079 | 435 | 1,514 | 971 | 404 | 1,375 | |||||||||||||||||||||||||

| Segment site rental cost of operations | 218 | 141 | 359 | 215 | 131 | 346 | |||||||||||||||||||||||||

| Segment services and other cost of operations | 143 | 2 | 145 | 115 | 1 | 116 | |||||||||||||||||||||||||

| Segment cost of operations(a)(b) | 361 | 143 | 504 | 330 | 132 | 462 | |||||||||||||||||||||||||

| Segment site rental gross margin(c) | 611 | 290 | 901 | 567 | 271 | 838 | |||||||||||||||||||||||||

| Segment services and other gross margin(c) | 107 | 2 | 109 | 74 | 1 | 75 | |||||||||||||||||||||||||

| Segment selling, general and administrative expenses(b) | 23 | 49 | 72 | 28 | 45 | 73 | |||||||||||||||||||||||||

| Segment operating profit(c) | 695 | 243 | 938 | 613 | 227 | 840 | |||||||||||||||||||||||||

| Other selling, general and administrative expenses(b) | $ | 56 | 56 | $ | 47 | 47 | |||||||||||||||||||||||||

| Stock-based compensation expense | 29 | 29 | 32 | 32 | |||||||||||||||||||||||||||

| Depreciation, amortization and accretion | 389 | 389 | 385 | 385 | |||||||||||||||||||||||||||

| Interest expense and amortization of deferred financing costs | 173 | 173 | 160 | 160 | |||||||||||||||||||||||||||

| Other (income) expenses to reconcile to income (loss) before income taxes(d) | 14 | 14 | 47 | 47 | |||||||||||||||||||||||||||

| Income (loss) before income taxes | $ | 277 | $ | 169 | |||||||||||||||||||||||||||

(a) Exclusive of depreciation, amortization and accretion shown separately.

(b) Segment cost of operations excludes (1) stock-based compensation expense of $7 million for both of the three months ended September 30, 2019 and 2018, and (2) prepaid lease purchase price adjustments of $5 million for both of the three months ended September 30, 2019 and 2018. Selling, general and administrative expenses exclude stock-based compensation expense of $22 million and $25 million for the three months ended September 30, 2019 and 2018, respectively.

(c) See “Non-GAAP Financial Measures, Segment Measures and Other Calculations” herein for a discussion of our definitions of segment site rental gross margin, segment services and other gross margin and segment operating profit.

(d) See condensed consolidated statement of operations for further information.

| SEGMENT OPERATING RESULTS | |||||||||||||||||||||||||||||||

| Nine Months Ended September 30, 2019 | Nine Months Ended September 30, 2018 | ||||||||||||||||||||||||||||||

| Towers | Fiber | Other | Consolidated Total | Towers | Fiber | Other | Consolidated Total | ||||||||||||||||||||||||

| Segment site rental revenues | $ | 2,451 | $ | 1,267 | $ | 3,718 | $ | 2,318 | $ | 1,189 | $ | 3,507 | |||||||||||||||||||

| Segment services and other revenues | 689 | 11 | 700 | 489 | 8 | 497 | |||||||||||||||||||||||||

| Segment revenues | 3,140 | 1,278 | 4,418 | 2,807 | 1,197 | 4,004 | |||||||||||||||||||||||||

| Segment site rental cost of operations | 647 | 418 | 1,065 | 641 | 388 | 1,029 | |||||||||||||||||||||||||

| Segment services and other cost of operations | 398 | 6 | 404 | 292 | 6 | 298 | |||||||||||||||||||||||||

| Segment cost of operations(a)(b) | 1,045 | 424 | 1,469 | 933 | 394 | 1,327 | |||||||||||||||||||||||||

| Segment site rental gross margin(c) | 1,804 | 849 | 2,653 | 1,677 | 801 | 2,478 | |||||||||||||||||||||||||

| Segment services and other gross margin(c) | 291 | 5 | 296 | 197 | 2 | 199 | |||||||||||||||||||||||||

| Segment selling, general and administrative expenses(b) | 73 | 147 | 220 | 81 | 131 | 212 | |||||||||||||||||||||||||

| Segment operating profit(c) | 2,022 | 707 | 2,729 | 1,793 | 672 | 2,465 | |||||||||||||||||||||||||

| Other selling, general and administrative expenses(b) | $ | 168 | 168 | $ | 141 | 141 | |||||||||||||||||||||||||

| Stock-based compensation expense | 90 | 90 | 84 | 84 | |||||||||||||||||||||||||||

| Depreciation, amortization and accretion | 1,176 | 1,176 | 1,138 | 1,138 | |||||||||||||||||||||||||||

| Interest expense and amortization of deferred financing costs | 510 | 510 | 478 | 478 | |||||||||||||||||||||||||||

| Other (income) expenses to reconcile to income (loss) before income taxes(d) | 41 | 41 | 153 | 153 | |||||||||||||||||||||||||||

| Income (loss) before income taxes | $ | 744 | $ | 471 | |||||||||||||||||||||||||||

(a) Exclusive of depreciation, amortization and accretion shown separately.

(b) Segment cost of operations excludes (1) stock-based compensation expense of $21 million and $19 million for the nine months ended September 30, 2019 and 2018, respectively, and (2) prepaid lease purchase price adjustments of $15 million for both of the nine months ended September 30, 2019 and 2018. Selling, general and administrative expenses exclude stock-based compensation expense of $69 million and $65 million for the nine months ended September 30, 2019 and 2018, respectively.

(c) See “Non-GAAP Financial Measures, Segment Measures and Other Calculations” herein for a discussion of our definitions of segment site rental gross margin, segment services and other gross margin and segment operating profit.

(d) See condensed consolidated statement of operations for further information.

Dan Schlanger, CFO

Ben Lowe, VP & Treasurer

Crown Castle International Corp.

713-570-3050